bank owned life insurance regulations

The bank may decide to offer a life insurance benefit only to the CEO the members of the executive team or the 20 top highest paid employees for example. The insureds are employees and the institution retains at least some interest in the death benefit proceeds.

2

Banking organization insurance programs include the funding of employee benefits through purchases of corporate- or bank-owned life insurance and the transfer of insurable risks through coverages associated with risk management initiatives.

. The death benefit proceeds follow this same model as long as banks abide by federal rules governing the use of BOLI. Similar to these there is also Credit Union-Owned. The bank pays the premium owns the cash value of the policies and is the beneficiary of the insurance.

Both pay benefits to the employer or directly to the employees families. Section 24 of the Federal. Bank-owned life insurance BOLI is a form of life insurance used in the banking industry.

Bank-owned life insurance BOLI is a type of permanent life insurance policy banks buy for high-salaried employees or board members. BOLI and other forms of life insurance investments provide tax-exempt income if the policy is held until the. Banks use it as a tax shelter and to.

COLI is life insurance on employees lives that is owned by any corporate employer. The bank purchases life insurance on the lives of a group of employees such as executives and officers that participate in the banks benefit plans. Purchase and Risk Management of Life Insurance to institutions to help ensure that their risk management processes for bank-owned life insurance BOLI are consistent with safe and sound banking practices.

Cash surrender values grow tax-deferred providing the bank with monthly bookable income. Of the many tax law changes enacted as part of the Tax Cuts and Jobs Act of 2017 TCJA one provision is raising concern among banks involved in certain post-2017 acquisitions of target banks with ownership in bank-owned life insurance BOLI policies. Some state laws permit state-chartered banks to engage in activities including making investments that go beyond the authority of a national bank.

A form of permanent life insurance owned by banks to offset the future costs of providing employee benefits. Community Reinvestment Act CRA Consumer Compliance. Bank owned life insurance BOLI is life insurance purchased and owned by banks.

The interagency statement also provides guidance for split-dollar arrangements and the use of life insurance as security for loans. Bank Owned Life Insurance BOLI is a tax efficient method that offsets employee benefit costs. Cash surrender values are allowed to grow tax-deferred to provide the bank with monthly bookable income.

The Office of the Comptroller of the Currency the Board of Governors of the Federal Reserve System the Federal Deposit Insurance Corporation and the Office of Thrift Supervision have issued the attached interagency statement on bank-owned life insurance BOLI to remind financial institutions that the purchase and risk management of BOLI must be. Bank-owned life insurance is a type of life insurance bought by banks as a tax shelter leveraging tax-free savings provisions to fund employee benefits. The buildup of cash surrender value within the policy is included in book earnings but excluded from the calculation of federal taxable income.

Risk management processes for bank-owned life insurance BOLI are consistent with safe and sound banking practices. Upon the executives death tax-free death benefits are paid. The bank is the owner of the policies pays all premiums typically a single lump-sum premium and is the beneficiary of the insurance proceeds.

The general rule for bank-owned life insurance BOLI is that proceeds received by reason of death are tax free. Banks can purchase BOLI policies in connection with employee compensation and benefit plans key person insurance insurance to recover the cost of providing pre- and post-retirement employee benefits insurance on borrowers and. The primary benefit of BOLI is its treatment for corporate income tax purposes.

The permanent policies accrue cash value which earns tax. Bank-Owned Life InsuranceInteragency Statement on the Purchase and Risk Management of Life Insurance. Written consent is obtained from all individuals to be insured.

Some banks may choose to share a portion of these proceeds with plan participants. BOLI is a tax-efficient tool often used to offset the cost of an employee benefit program making it easier for banks to. Bank-owned life insurance BOLI policies is one life insurance type typically taken out on key employees of a company.

Financial institutions supervised by the Federal Reserve also engage in functionally regulated insurance. The purpose of this guidance letter is to clarify the New York State Banking Departments the Departments position on Bank Owned Life Insurance BOLI programs. With the exception of term policies occasionally used to cover a borrower while a large debt remains outstanding bank-owned policies are usually permanent life insurance like whole or universal life.

A bank will purchase and own a life insurance policy on an executive or group of executives lives and the bank is listed as the beneficiary of the policy. The federal banking agencies are providing guidance on the safe and sound banking practices they expect institutions to employ for the purchase and ongoing risk management of bank-owned life insurance. The Interagency Statement on the Purchase and Risk Management of Life Insurance OCC 2004-56 provides general guidance for banks and savings associations regarding supervisory expectations for the purchase and risk management for Bank Owned Life Insurance BOLIAmong the conservative banking practices discussed in this interagency statement is.

Its not a regular term. We dont need to add a life insurance benefit The point of BOLI is not life insurance coverage yes we know its called bank-owned life insurance. The interagency statement also provides guidance for.

Industry Letters Guidance on Bank Owned Life Insurance BOLI Programs January 6 2003 TO THE CHIEF EXECUTIVE OFFICER OF THE INSTITUTION ADDRESSED. The bank pays for the coverage and is the beneficiary after the insured persons death. The bank purchases and owns an insurance policy on an executives life and is the beneficiary.

This letter also provides general guidance to. When the insured executive passes away the tax-free death benefits are paid to the. However if the BOLI policy is transferred for value ie the purchase of an existing policy rather than a newly issued policy the death benefit is no longer tax free unless an exception applies to the transfer.

BOLI is the acronym for Bank Owned Life Insurance. National banks may purchase and hold certain types of life insurance called bank-owned life insurance BOLI under 12 USC 24 Seventh. Bank Owned Life Insurance BOLI is essentially the same as COLI but the life insurance policy is purchased and owned by a bank.

Upon death the bank will be awarded tax-free death benefits and any cash. When structured correctly BOLIs favorable assetsliabilities timing. Bank-owned Life Insurance BOLI Interest Rate Risk.

Since the bank is the beneficiary the life insurance policy provides protection for the bank if the covered employees were to pass away unexpectedly. The bank purchases life insurance on a select group of management including officers or other key personnel.

Cross Selling Unlocking The Value In Bancassurance

2

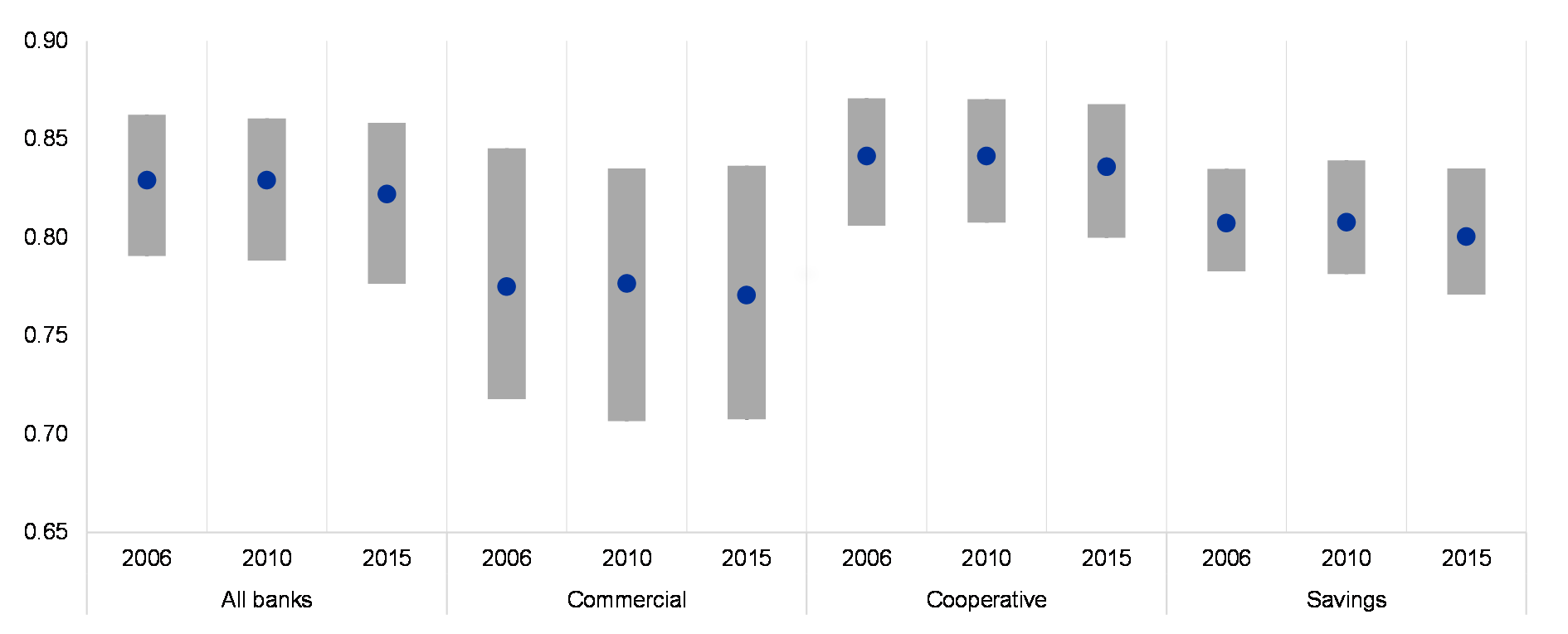

Financial Stability Review May 2018

:max_bytes(150000):strip_icc()/hsbc-branch-in-new-bond-street--london-533780165-ff99ebc393c243cba463ea80559836b0.jpg)

Bank Owned Life Insurance Boli

Bank Owned Life Insurance Boli

Financial Stability Review May 2018

2

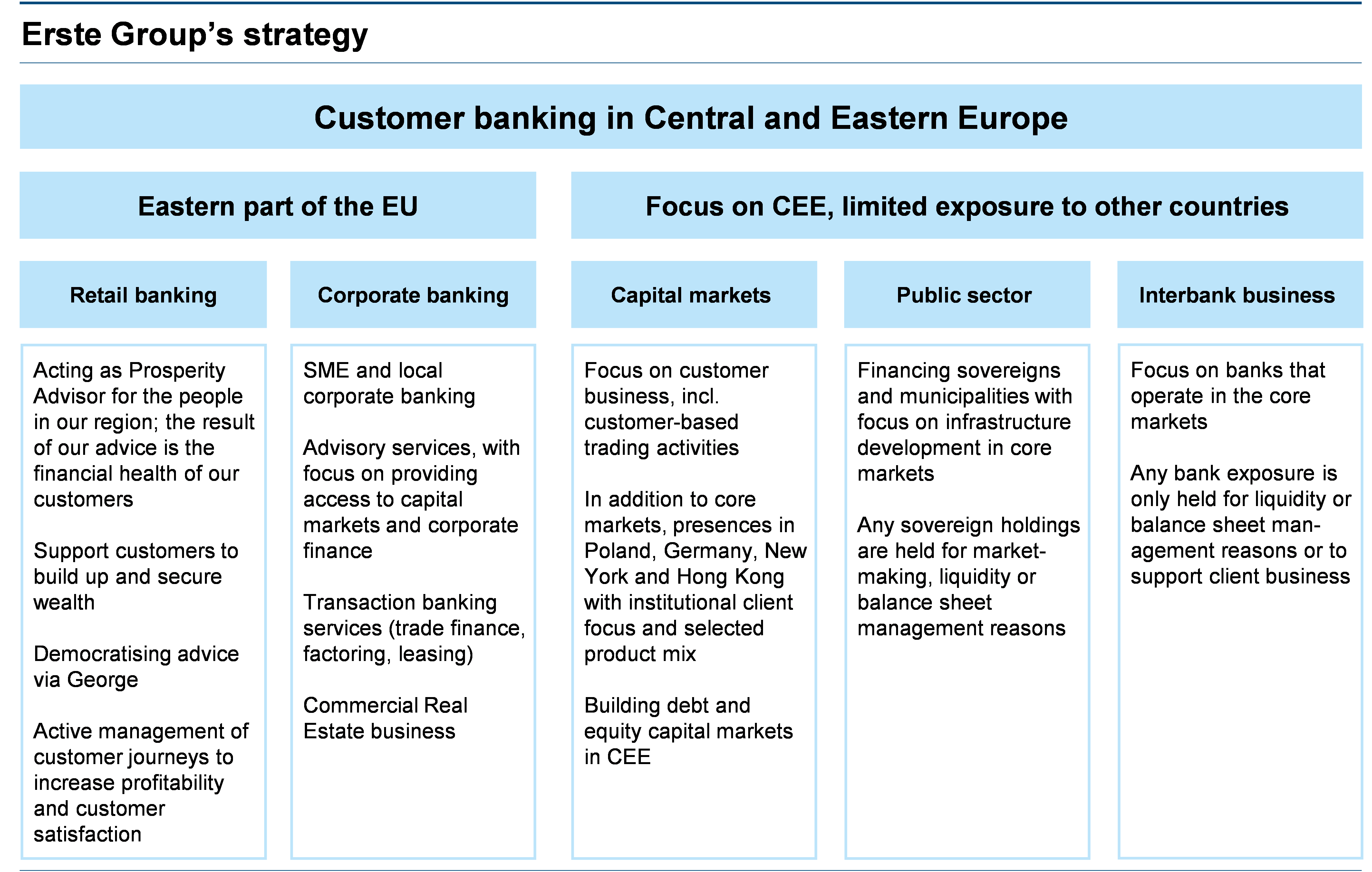

About Us Erste Group Bank Ag

:max_bytes(150000):strip_icc()/dotdash-insurance-companies-vs-banks-separate-and-not-equal-Final-9323c943f9974aad96b2c70d6e3aa577.jpg)

Insurance Companies Vs Banks What S The Difference

:max_bytes(150000):strip_icc()/P2-ThomasCatalano-d5607267f385443798ae950ece178afd.jpg)

Bank Owned Life Insurance Boli

Insurance Europe

Understanding Life Insurance Policy Ownership The American College Of Trust And Estate Counsel

New Pension Fund Statistics

Security News Trending Topics It Security Myra Security

Financial Stability Review May 2018

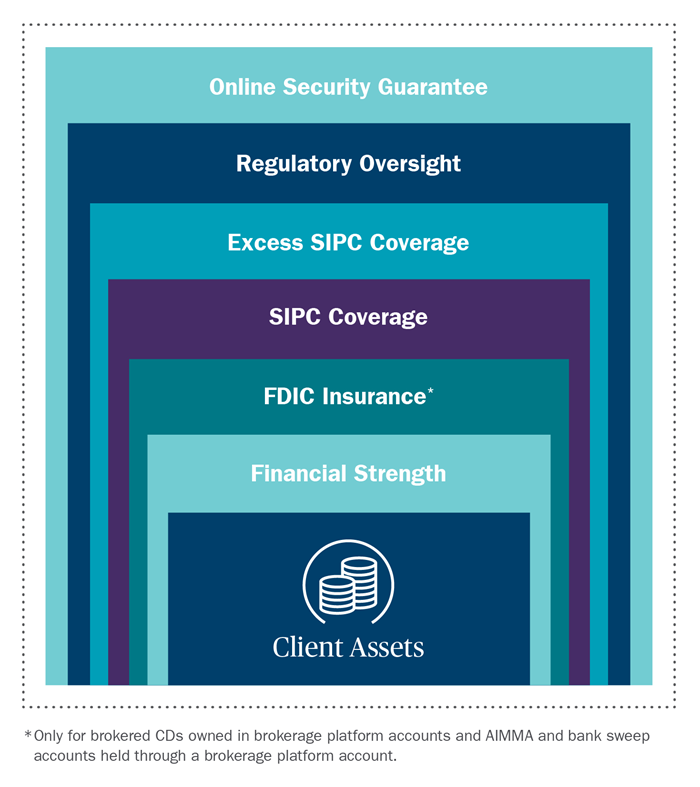

Understanding Sipc And Fdic Coverage Ameriprise Financial

2

2

Full Article Life Insurance Demand Analysis Evidence From Visegrad Group Countries